Removing the Biggest Hurdles to Plan Participation

Traditional Employee Stock Purchase Plans (or ESPPs) in the U.S. are on the verge of benefitting from a major enhancement thanks to the ingenuity of Carver Edison, a creative newcomer to the equity compensation industry. Carver Edison is a New York City-based financial technology company committed to improving ESPP participation while creating value for employers. Specifically, Carver Edison has solved for the biggest problem that rank-and-file employees face when it comes to ESPP participation: the lack of available funds to contribute to payroll deductions.

Carver Edison provides employees of publicly traded companies with interest-free ESPP participation loans, thereby eliminating the issue of a lack of available funds. The advantage is three-fold:

- Employees benefit by owning and holding more shares long-term for the same economic experience as a traditional ESPP

- Companies benefit by increased engagement, cash flow and tax savings

- Shareholders benefit from the increased “owner mentality” and greater employee alignment

Additionally, Carver Edison has obtained a private letter ruling from the IRS affirming that plan sponsors are able to maintain the qualified tax status afforded in Section 423 while utilizing the services that Carver Edison provides.

Purpose of this Paper

Aon has partnered with Carver Edison to aid plan sponsors in understanding the impact to financial reporting, tax accounting and company balance sheet of a Carver Edison ESPP as compared to a traditional ESPP.

Employee Example

Many employees at companies that sponsor traditional ESPPs are unable to afford the payroll deductions needed to fully participate. In fact, many eligible employees do not participate at all due to cash constraints. Carver Edison solves this problem by enabling employees to maximize their ESPP contributions without requiring an increase in their payroll deductions. The employee determines how much he or she wants to contribute to the plan out of salary deductions. Carver Edison provides the interest-free loan for the remainder, up to the maximum contribution allowed by the Income Tax Code (or Plan, if applicable) directly to the issuer on behalf of the employe. The accompanying table illustrates the percent of the ESPP contribution that would be provided by a Carver Edison interest-free loan for a plan that allows a 10% maximum contribution.

Most plans offer an opportunity for employees to purchase their employer stock at a discount. The combination of the employee’s contributions together with Carver Edison’s interest-free loan is used to purchase shares at the discount. On the date the shares are purchased from the ESPP, Carver Edison sells enough shares to repay the amount of the loan (the “Loan Repayment Shares”). Under a Carver Edison plan, the employee will own more long shares outright and will enjoy higher gains than a traditional ESPP [1].

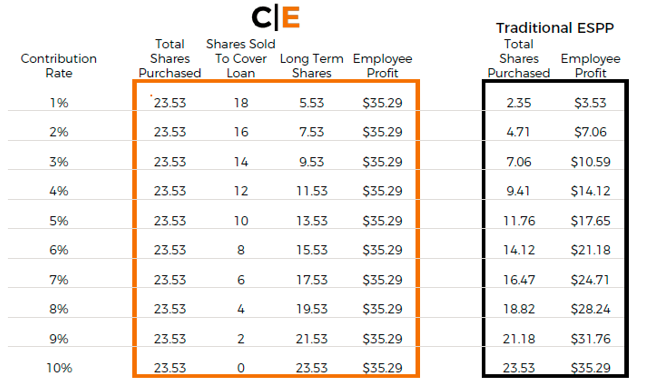

The table below compares the gain realized by the participant of a Carver Edison ESPP under different levels of employee contributions with the gain the employee would realize under a traditional ESPP.

The examples assume:

- The level of employee contributions varies from 1% to 10%

- The employee is eligible to contribute up to $200

- The stock price equals $10

- Shares are purchased at a 15% discount

[1] ESPPs may vary from company to company. While a 15% discount and a “look-back” to the beginning of the enrollment period are often typical, discounts vary from 5% to 15% and the plan may or may not provide for a look-back.

Under a Carver Edison plan, the employee can contribute the full $200 regardless of the level of payroll deductions the employee can afford, resulting in the maximum number of shares (23.53 shares) being purchased in all scenarios and $35.29 of gain being realized in all scenarios. By contrast, under the traditional ESPP, if the participant is unable to contribute the full 10% through payroll deductions, the employee’s benefit can be materially reduced.

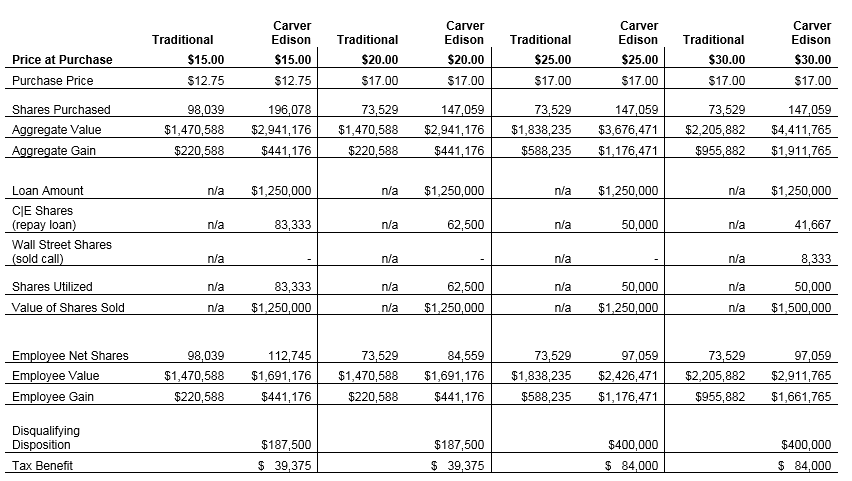

In exchange for this additional benefit, the employee agrees to cap the potential gain for the Loan Repayment Shares at a pre-determined stock price increase (e.g., 25% growth during offering period). For example, in the illustration above, if the stock price equaled $10 on the first day of the offering period and equaled $14 on the date the shares were purchased, the amount of the interest-free loan would be divided by $12.50 (the $10 initial stock price plus the 25% appreciation cap) to determine the number of shares that must be sold. If the price of the company’s stock doesn’t increase by more than 25% during the deferral period, there is no appreciation cap and hence no opportunity cost to the employee. If the stock price does increase by more than 25% during the deferral period, the participant would have an opportunity cost such that the gain in the example would be capped at $2.50 per share with respect to the Loan Repayment Shares.

Carver Edison generates revenue by selling options to financial institutions that allows the financial institutions to realize the benefit of the stock price exceeding the 25% cap ($12.50 in the above example) on the Loan Repayment Shares. Carver Edison also uses the proceeds from selling the option to cover the cost of the financial transactions, employee education and services provided to the plan sponsor. In the above example, the employee receives the full benefits of the ESPP in all scenarios in which the stock price has not increased more than 25% and foregoes the opportunity that the stock will rise above 25% for the Loan Repayment Shares.

Financial Reporting Implications

We believe a Carver Edison ESPP will significantly increase participation rates among employees and increase the total number of shares purchased by employees. These will have a direct impact on the financial reporting through higher estimated contributions and actual shares purchased. However, the actual impact to expense, tax accounting and dilution is more nuanced and not proportional to the increase in contributions. We will examine the impact on the accounting value per share, aggregate expense, tax accounting (i.e., disqualifying deductions) and balance sheet (cash flow and dilution).

Impact on the Accounting Value Per Share

For companies that adopt a Carver Edison ESPP, the interest-free loan and the 25% appreciation cap on the Loan Repayment Shares are features of the plan. Therefore, the impact of the 25% appreciation cap needs to be reflected in the accounting value of the shares that are purchased with the interest-free loan. This will result in a bifurcated approach for determining the fair value and eventual expense between a share that is issued under a traditional ESPP and a share that is issued under a Carver Edison ESPP.

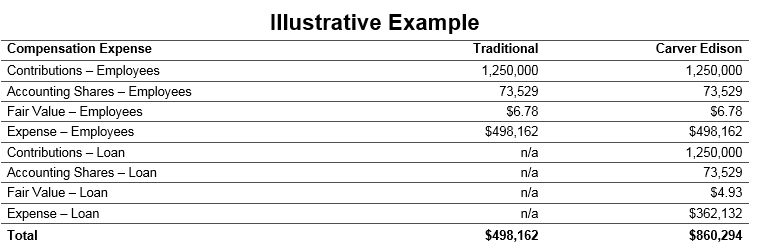

Companies recognize compensation expense for every share that is issued under an ESPP. If participation increases under a Carver Edison plan, the amount of compensation expense will likewise increase. However, the shares that are purchased with the Carver Edison interest-free loan will be less expensive to the issuer than the shares that are purchased through traditional ESPPs. The financial accounting value of a share issued under a traditional ESPP with a 15% discount and look-back consist of 4 components:

- 15.0% of the price of a share of stock on the first day of the offering period (captures value of discount)

- 85% of an at-market call option (captures value of look-back when price goes up)

- 15% of an at-market put option (captures value of look-back when price goes down)

- Foregone interest (captures the opportunity cost of the participant payroll deferrals during the period not accruing interest during the period between the deferral and the shares being purchased)

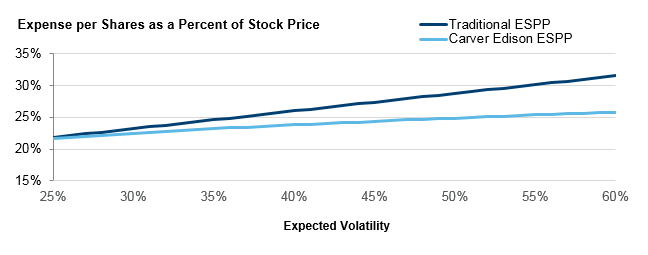

The impact of the 25% appreciation cap on the accounting value per share is captured by subtracting the value of an out-of-the-money call option that is priced at a 25% premium. Because the 25% appreciation cap only applies to the Loan Repayment Shares, rather than to all of the shares purchased with the interest-free loan, the value of the out-of-the money call receives a 68% weighting (1 – the 15% purchase discount) / (1 + the appreciation cap) = 85% / 125% = 68%). The chart below illustrates the expense per share for a share that is purchased with a Carver Edison loan and a share that is purchased under a traditional ESPP. To allow for comparability, the expense is expressed as a percent of stock price.

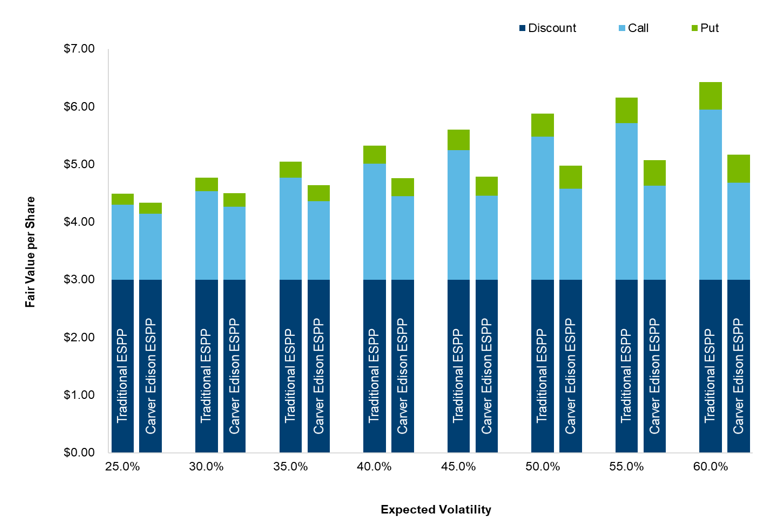

The following table illustrates the fair value components for a company with a $20 offering price and 15% discount with a look-back.

Income Statement Impact

We noted above that a Carver Edison ESPP will increase employee participation and the total amount of funds available for purchase (i.e., employee contributions plus interest-free loan). The higher total amount contributed will increase the compensation expense recorded. The increase will not be proportional because the contributions facilitated by the loan will have a lower fair value. There will also be a partial offset for most companies due to corporate tax savings (i.e., higher disqualifying dispositions triggered by the immediate sale of the Loan Repayment Shares).

To illustrate the income statement impact at Company ABC, we have further assumed all employees contribute 5% under the traditional ESPP and take an additional 5% loan (10% total) under the Carver Edison plan. The expense per 6-month purchase period is as follows:

We examined several future stock price scenarios to illustrate the gain to participants and capture the additional tax benefit to the company.

Please note we have ignored disqualifying dispositions that are likely to occur due to an employee selling shares, and only shown the direct impact of the disqualifying disposition of the Loan Repayment Shares.

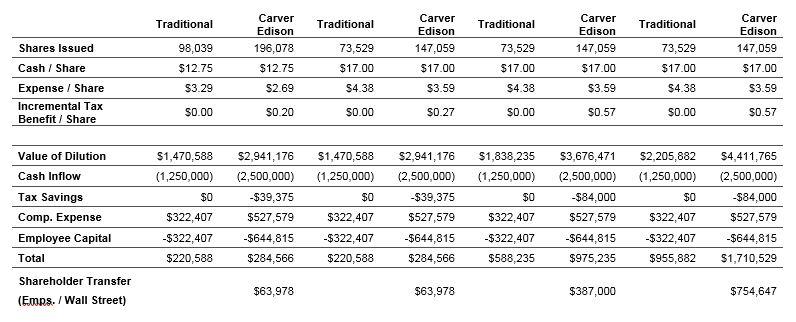

Balance Sheet Impact

Plan sponsors of a Carver Edison ESPP will see an increase of cash inflow equal to the amount of the interest-free loan and an increase in dilution due to the additional shares purchased. The compensation expense and tax benefit discussed above will flow through the income statement with the balance residing in Additional Paid in Capital (APIC).

Reporting of Tax Basis

The immediate sale of the Loan Repayment Shares will result in a disqualifying disposition. To the extent the price of the company’s stock has appreciated since the first day of the offering period, the employee will have short-term capital gain on the excess of the stock price at the time of sale over the stock price on the first day of the offering period. If the stock price has appreciated by more than 25%, the gain realized by the employee will not match the amount of the appreciation at the time the shares are sold. For example, if the stock price on the first day of the offering period and at the time of sale equaled $10 and $14 respectively, the aggregate gain would equal $4, but the employee’s gain is capped at $2.50. Fortunately, the 25% cap is considered a non-lapse restriction under Internal Revenue Code § 83. As a result, the amount of gain on which the employee will be subject to tax will also be capped at 25% appreciation. The employee will not be subject to tax on the foregone gain if the price of the company’s stock at the time the Loan Repayment Shares are sold has appreciated by more than 25%.

Conclusion

A Carver Edison plan is a force multiplier for traditional ESPPs that removes what has historically been one of the biggest hurdles to participation: the employees’ ability to afford to defer compensation to purchase the shares. A Carver Edison plan will allow companies to more fully realize the goals for the plan. Under a Carver Edison plan, employees benefit by owning and holding more shares long-term; companies benefit by increased engagement, cash flow and tax savings; and shareholders benefit from the increased “owner mentality” and greater employee alignment. Additionally, the compensation expense for a share purchased with a Carver Edison interest-free loan is generally lower than the expense for a share issued under a traditional ESPP.

Related Articles