With the clock ticking on the January 2018 implementation date for the CEO pay ratio— and no action taken by the SEC yet to delay the rule— here’s how companies should prepare.

As we move past the midpoint of 2017, work is already underway at a number of our clients to begin preparing for the calculation and disclosure of CEO pay ratios next spring. Although many experts had anticipated the CEO pay ratio rule would be delayed or repealed as part of a broader rollback of the Dodd-Frank Act by a Republican congress, this is now looking increasingly unlikely, and companies and advisors across all industries are now resuming preparations to comply in 2018.

For some companies, the process of calculating and disclosing their CEO pay ratio will be far more complex than they assume. And for all issuers, the disclosure is potentially controversial and should be addressed with appropriate diligence, especially in the first year of implementation. Below are the key steps we recommend taking to ensure your organization stays on track:

Review (again) the SEC’s interpretative guidance issued last fall.

The SEC’s guidance addresses several important details that are critical to proper implementation of the CEO pay ratio rule, including:

- What employees can/should be included in the population from which the “median” employee will be identified?

- What is the range of appropriate/allowable “consistently applied compensation measures” (CACM), which can be used to identify the median employee?

- What is the period to be used in calculating a CACM?

Do one or more trial runs of your analysis to understand how your CEO pay ratio changes as you select from the range of approved methodologies.

This is an important step since the SEC’s guidance clearly indicates that companies will have significant flexibility in how to determine their ratios to minimize the burden of compliance and produce as meaningful a result as possible. It will also be important to consider the longer-term implications of the choice made for 2018, as stakeholders will expect you to use a consistent methodology year-over-year. It may be preferable to use a methodology similar to your peers to avoid controversy about how your number was calculated and this will bring more fairness to the comparisons that will inevitably be made between you and your competitors.

Learn how to put your CEO pay ratio into the right context.

To do this, companies will need to assess how their own CEO pay ratio stacks up to the ratios of their peers. Understanding what is an “expected” range of ratios in your industry, and what types of factors might justify being higher or lower in the range, will be critical when it comes to drafting meaningful disclosure, including an explanation of the ratio in your proxy statement.

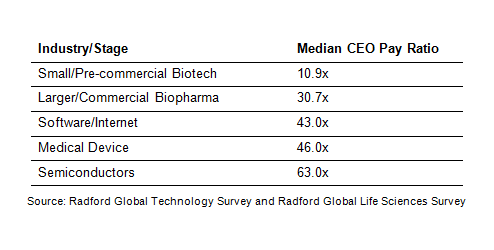

Last year, as the table below illustrates, we completed preliminary research on CEO pay ratio outcomes by industry, and we continue to conduct custom research for many clients as we prepare for 2018. Early findings indicate that smaller biotech companies, which tend to have knowledge-based workforces mostly in higher-cost countries, often have quite low CEO pay ratios compared to other sectors. Larger commercial biotech firms with manufacturing operations tend to have higher ratios, followed by software and Internet companies, medical device, and finally semiconductor companies, which often have large offshore manufacturing operations that can yield low “median employee” pay levels. For more information, see our article: In Calculating Your CEO Pay Ratio, Relativity to Peers is the New Math.

Start thinking about your actual disclosure.

Start thinking about your actual disclosure.

While most companies won’t begin drafting their Compensation Discussion & Analysis (CD&A) in earnest until the spring, we recommend that clients get an early start on their CEO pay ratio section since it will be brand new. While it is unclear to what degree institutional investors or proxy advisors will use CEO pay ratio disclosures, we fully expect these ratios to be a point of focus for labor groups and the media. As a result, companies will want to consider providing supplementary narrative discussion with additional context for their ratio. This could include a review of market and peer trends similar to those described at a high level above, and discussion of where and why a company is positioned relative to its peers. Crafting a compelling story around the pay ratio will be an important project that should include input from both internal stakeholders and key advisors and consultants, and is best begun sooner rather than later in our opinion.

While many companies are focused on the logistics of calculating and drafting the disclosure around their CEO pay ratio, don’t neglect to think through the story you plan to tell and how that message will resonate with all of the different stakeholders who might read your disclosure. For example, your investors might use the pay ratio to make investment and proxy voting decisions; employees, on the other hand, might be interested in how their own pay compares to the median worker. Prepare in advance for any questions from stakeholders that may arise so you’re not caught off guard when proxy season comes.

To speak with a member of our compensation consulting team regarding CEO pay ratios or any other executive compensation topics, please write to consulting@radford.com.

Related Articles