As executive compensation planning season kicks off, and another proxy season looms, we look back at this year's Say-on-Pay results and lessons learned.

Now that a sixth year of Say-on-Pay voting for life sciences companies has come and gone, and as many companies begin to assess their executive compensation programs for 2017, the consulting team at Radford decided to take a look back at the biggest takeaways from the 2016 Say-on-Pay voting season.

Download our full say-on-pay voting results for the life sciences sector here.

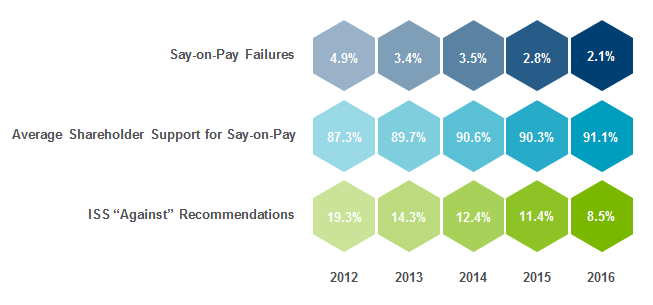

Within the life sciences sector, average support levels have risen slightly year-over-year, from 90.3% in calendar year 2015 to 91.1% in 2016 to-date (data pulled from annual meetings held January 1 to May 31, 2016). Meanwhile, Institutional Shareholder Services (ISS) is recommending in favor of life sciences' Say-on-Pay votes at record high rates— "Against" recommendations are down one-third from 11.4% in 2015 to 8.5% this year. ISS now supports life sciences' pay proposals at the same clip as for the broader Russell 3000, even though biotech companies are much more likely to deviate from ISS's published standards of best practices than companies in other industries.

The 2016 results reflect the continuation of a very favorable trend for life sciences companies. Outright failures on Say-on-Pay among life sciences companies have fallen steadily over the past five years, from 4.9% in 2012 to 2.1% this year, and are now roughly in line with failure rates in other industries.

At first glance, solid shareholder support for executive pay practices at life sciences companies may be surprising given the sector-wide downturn in stock performance over the past year. On a 12-month trailing basis ending May 30, 2016, one-year total shareholder return (TSR) in the biopharma sector is -30%, compared to -5% for the Russell 3000 over the same period. Yet, our work with life sciences sector clients reveals several explanations for the robust support of pay programs during a year of poor stock price returns. First, many companies in the biotech and medical device industries continue to take steps to enhance alignment between the design of their pay programs and ISS and investor "best practices" particularly in instances where doing so has a limited impact on their ability to effectively manage compensation programs to achieve short- and long-term strategic objectives. This dramatically reduces the likelihood that shareholders will raise alarm bells about pay or governance practices, even during periods of poor stock performance. We also continue to see strong adoption of enhanced compensation disclosures and proactive shareholder engagement on compensation and governance issues across the life sciences sector.

Our experience suggests this type of engagement works, and can often counteract the effect of a negative ISS Say-on-Pay vote recommendation. As boards and management teams become more responsive to investors' concerns and take greater pains to explain the rationale behind pay programs— especially those that aren't in line with so-called best practices— shareholders appear more and more willing to support their pay programs. This last point is particularly critical for life sciences companies where business practices and competitive concerns necessitate design choices like shorter performance cycles and heavier use of stock options that differ from what many proxy advisors and broad-based investors' voting policies might prescribe.

To get a better idea of what's driving these numbers, Radford conducted a detailed review of compensation practices among two subsets of life sciences companies: (1) Companies with below 70% support for their 2016 Say-on-Pay vote, and (2) Companies that improved their Say-on-Pay vote by 35% or more from 2015 to 2016.

Among the companies with shareholder support levels below the 70% threshold, we were interested in identifying the primary factors driving shareholder opposition to Say-on-Pay. Our research uncovered the following:

- A perceived disconnect between pay and performance: typically TSR performance below a peer group median or declines in absolute performance while compensation increased, stayed the same or didn't decrease enough

- "Poor" incentive pay practices, including above-target payouts despite perceived poor performance, short performance periods for long-term incentive awards, lack of predominantly performance-based programs

- Poor disclosure, including a lack of detailed discussion on linking payouts under variable incentive programs to corporate and/or individual performance

- Lack of responsiveness to prior year concerns

It should be noted that there may be valid reasons for companies in the life sciences space to make these design choices, and that detailed disclosure and proactive shareholder engagement can go a long way toward assuring shareholders that the program is aligned with their long-term interests and deserving of their support.

Our second subset of companies that improved their vote took substantive actions to align their programs with investor "best practices". The most commonly observed initiatives include:

- Holding meetings and organized dialogue/ engagement with shareholders, often representing up to 60% of the total shareholder base

- Changing equity incentive mixes to include a greater emphasis on vehicles with performance-based vesting

- Adding new performance metrics to existing equity incentive plans, including relative total shareholder return (TSR) and return on invested capital (ROIC)

- Extending performance periods for cash and/or equity incentives (moving from one-year performance periods to two or three years)

- Developing enhanced disclosure of your process for setting short-term incentive goals and determining payout levels

Stock Incentive Plan Proposals

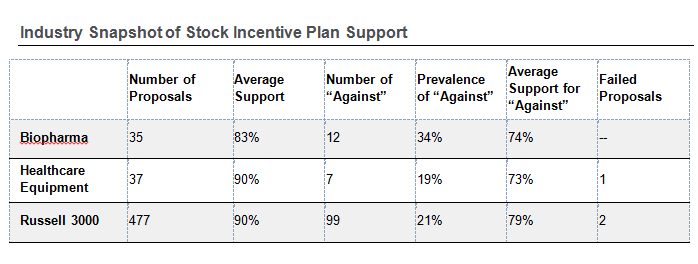

We also examined shareholder voting results for stock incentive plan proposals in 2016. Requests to approve or replenish stock incentive plans are a staple of annual meetings, particularly in the life sciences sector, which relies heavily on equity incentives to attract, motivate and retain talent in a competitive market. While the vast majority of these proposals pass, they have received increased scrutiny in recent years amid shareholder concerns about burn rates and total dilution. ISS, which exerts considerable influence on these votes, overhauled the way it evaluates proposals during the 2015 proxy season and continues to make tweaks to its process. (You can read our client alert on initial ISS changes for 2015 here followed by updates for the 2016 season here.)

There was little year over year movement in the rate of ISS or shareholder support for stock incentive plan proposals in 2016. The primary takeaway is that the biopharmaceuticals sub-industry continues to receive significantly more ISS "no" votes than the broader Russell 3000 (or medical device sub-industry, where equity use is comparatively modest). Nonetheless, while ISS has yet to catch up with biopharmaceuticals sector practice, shareholders appear to understand the industry, supporting stock incentive plan requests in this sector at a level only modestly below the average level of support in the Russell 3000.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.

Related Articles