ISS tweaked its equity plan scorecard, made changes to the number of outside boards directors are advised to serve on, and updated its governance guidelines for IPO companies.

As part of its annual Policy Updates, Institutional Shareholder Services, Inc. ("ISS") announced changes to its ISS equity plan proxy voting policy and to several corporate governance policies for the upcoming 2016 proxy season. Additionally, ISS released notification regarding its annual proxy peer submission process and its equity data verification portal. These policy updates are effective for annual meetings held on or after February 1, 2016. The following paragraphs highlight the key policy changes for the 2016 proxy season.

Equity Plan Scorecard Updates

While the basic Equity Plan Scorecard ("EPSC") policy has not changed, ISS made a few modifications to the EPSC evaluation framework. These changes include the addition of a model for newly IPO (or emerging from bankruptcy) large cap companies, and adjustments to the scorecard factors with respect to holding period requirements and change-in-control ("CIC") equity vesting. We have summarized below the most important updates relating to EPSC model.

New Model for Large Cap New IPO Companies

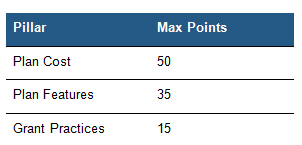

ISS renamed the current IPO model to "Special Cases" model and created a new Special Cases model for newly IPO Russell 3000/S&P 500 companies. The Special Cases model for Russell 3000/S&P500 companies includes all Grant Practices factors except Burn Rate and Share Pool Duration. The maximum pillar scores for this model are as follows:

Prior to the update, ISS analyzed all newly IPO (or merging from bankruptcy) large cap companies using the old IPO model (i.e., no Grant Practices factors apply). With the creation of these two additional models, ISS now has five EPSC models based on the type and status of the company being evaluated: (i) S&P 500; (ii) Russell 3000 index (excluding S&P 500 companies); (iii) Non-Russell 3000; (iv) Special Cases (recent IPOs or bankruptcy emergent companies, or any company that does not disclose at least three years of grant data) for non-Russell companies; and (v) Special Cases for Russell 3000/S&P 500.

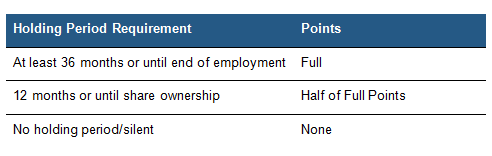

New Scoring for Holding Period Requirement

ISS increased the post vesting/exercise holding period requirement to receive full points under the model from 12 months to 36 months or until employment termination. A holding period requirement of 12 months or until stock ownership guidelines are met will continue to receive half points under the revised model. Previously, a holding period of at least 12 months resulted in full points under the old scorecard model.

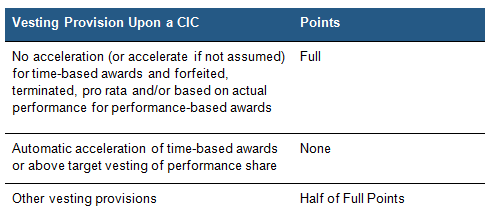

New Scoring for CIC Equity Vesting Provision

ISS renamed the "Automatic Single-Trigger Vesting" plan features factor to "CIC Vesting" and modified the scoring levels to take into consideration the treatment of performance-based awards in the event of a CIC. The scoring is as follows:

Prior to the update, ISS awarded full points as long as equity awards did not auto-accelerate upon a CIC. No partial points were awarded under the old model.

Scoring Adjustments for Certain Factors

ISS also made some modifications with respect to the point allocations for certain factors. However, the specific adjustments were not publicly disclosed. The threshold of 53 points to receive a favorable recommendation (absent egregious factors) remains unchanged.

Aon Hewitt Comment: Overall, the 2016 EPSC updates appear generally minor in nature, except with respect to the creation of the new Special Cases for Russell 3000 and S&P 500 companies. This move is somewhat expected as most investors typically regard large cap IPO companies as already having robust grant practices at IPO, compared to smaller cap new IPO companies.

The three-year holding period requirement (versus one-year) will likely discourage some companies from adopting such practice as it may be perceived as a more substantial burden to the CEO or other participating NEOs to hold the shares for three years post vesting/exercise. However, some external observers have indicated that companies may move to adopt such post vest holding periods for three years to align with the lookback period under the anticipated final Dodd Frank clawback rules. However, in the immediate future, we anticipate that companies will continue to adopt the "middle ground" for this particular input which is the implementation of a retention ratio until stock ownership guidelines are met, which will continue to receive half points under the revised model.

With respect to the CIC vesting factor, the updated policy will force companies to specifically address the treatment of performance-based awards in the event of a CIC in order to potentially receive maximum points for this factor. Since this appears to be a higher scored data point, we expect companies to start complying with this requirement to obtain maximum points for this input.

Lastly, while ISS has removed the "excessive" shareholder value transfer cost and burn rate cost factor from the Overriding Factors policy, we still anticipate that negative scoring associated with such factors will make it difficult for some companies to ultimately seek shares and obtain a passing score.

Overboarding

For CEOs of public issuers, ISS has retained its current policy of recommending against/withhold for CEO directors sitting on more than two public companies besides their own board. Note: ISS will not issue the negative vote recommendation towards the overboarded CEO’s company specific nomination but solely towards the other board nominations. ISS has stated that it intends to continue to study the issue and may reconsider it in the future.

For other non-CEO directors, ISS will note in its report if a director serves on more than five public company boards during 2016, but will only recommend that shareholders vote against directors who sit on more than six public company boards. However, starting on or after February 1, 2017, negative recommendations will be made for non-CEO directors sitting on more than five public company boards.

Contrast these policy changes with the more aggressive ones that have been implemented by Glass Lewis for 2017. Specifically, beginning in 2017, Glass Lewis will recommend voting against a director who is an "executive officer" of a public company (not just the CEO) and sits on more than two public company boards or "non-executive officer" directors who serve on more than five public company boards.

Aon Hewitt Comment: While becoming more restrictive for non-CEO directors in terms of flexibility regarding the number of board memberships that can be maintained before negative vote recommendations are issued, the ISS approach is still less restrictive in comparison to the newly published Glass Lewis guidelines (especially for "executive officers," who can only serve on an aggregate total of two boards under the new policy). This is ultimately an area that issuers should analyze their top investor policies for exposure, as many investors have their own guidelines on the acceptable number of board memberships.

Unilateral Bylaw and Charter Changes

Currently, ISS’s existing policy recommends that its subscribers vote against/withhold director nominees, certain committees, or the entire board if the board amends company bylaws or charter without shareholder approval in a way that materially diminishes shareholder rights. ISS now bifurcates its analysis as to how it evaluates newly public companies and companies with a longer trading history.

For Existing Public Companies

ISS is largely concerned about an increase in the type and number of unilateral adoptions, with only 10 in 2013 and 64 and 62 for 2014 and 2015, respectively. As a result, taking into account the same factors used in previous years to assess whether to support or recommend against a company, ISS has indicated it is likely to recommend against boards that amended bylaws or charters to:

- Classify the board

- Adopt supermajority vote requirements, or

- To eliminate the shareholder’s ability to amend bylaws

Unless the adverse amendment is reversed or submitted to a binding shareholder vote, in subsequent years ISS will generally continue to recommend a vote against directors (although the policy also suggests ISS will also consider on a case-by-case basis whether to continue recommending against votes).

For Newly Public Companies

ISS will evaluate whether to recommend against directors based on the following factors:

- The level of impairment of shareholders’ rights caused by the provision

- The company’s or the board’s rationale for adopting the provision

- The provision’s impact on the ability to change the governance structure in the future (such as, limitations on shareholder right to amend the bylaws or charter, or supermajority vote requirements to amend the bylaws or charter)

- The ability of shareholders to hold directors accountable through annual director elections, or whether the company has a classified board structure

- A public commitment to put the provision to a shareholder vote within three years of the date of the initial public offering

Additionally, ISS has indicated that in subsequent years unless the adverse provision is reversed or submitted to a vote of public shareholders, it will base its vote recommendations for directors on a case-by- case basis. Note: Significant weight will be given to the shareholders’ ability to amend the governance structure in future years through simple majority (not supermajority) vote and non-classified boards. A public commitment by the company to put the adverse provision to a shareholder vote within three years of the IPO will be considered mitigating. Additionally, an IPO company may be able to avoid a negative recommendation altogether by including the commitment in the proxy statement for its first annual meeting.

Aon Hewitt Comment: Consistent with ISS policies on shareholder rights, any such material infringement that is acted upon unilaterally or at a minimum not put forth for a shareholder vote is almost always grounds for receiving negative vote recommendations. This latest policy update is aimed at expanding the application of protecting shareholder rights to newly public companies.

Compensation Practices of Externally Managed Issuers ("EMIs")

ISS will consider it a "problematic pay practice" if it believes that an EMI has failed to provide sufficient disclosure for shareholders to assess the compensation for named executive officers. EMIs typically do not disclose details about their compensation arrangements or payments made to executives by external managers, which ISS and its investor subscribers generally find problematic. Absent additional clarification regarding compensation arrangements, ISS could issue adverse vote recommendations for compensation related proxy ballot items, such as say-on-pay or compensation committee director nominees.

Aon Hewitt Comment: Consistent with the original intent of the revamped proxy disclosure rules, ISS continues to push for full and clear disclosure surrounding executive compensation programs and policies. Lack of robust (or in some cases any) disclosure is easily expected to trigger additional scrutiny, and oftentimes result in negative vote recommendations.

Overall, we will continue to monitor developments on ISS’s proxy voting guidelines and their application and will alert our client alert subscribers as soon as more information is available.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.

Related Articles