How private companies manage employee equity can be mysterious, but our analysis of changes based on a firm's age and level of investment reveals some interesting trends.

All private companies in the technology and life sciences sectors struggle with the same fundamental question: How much equity should we grant to our executives and broad-based employees?

This question is of utmost importance to private firms since they rely heavily on equity compensation in order to preserve cash and incentivize employees to remain with the company up to and beyond an IPO. Employees, for their part, have become savvier in determining the value of their option grants by asking questions like the size of proposed grants expressed as a percentage of total shares outstanding during the recruiting process.

While this may seem like a simple question, getting things wrong can have huge financial and human resources implications for employees and investors alike. Far too often, companies tackle this issue blindly without solid market data to back their decisions.

To provide a helping hand, we used recent data from the Radford Pre-IPO/Venture-Backed Survey, Radford Global Technology Survey, and Radford Global Life Sciences Survey to examine employee ownership levels and equity overhang rates at 388 US-based pre-IPO companies across two critical factors: company age and the amount of outside investment in a company. Using these two factors as an approximate gauge for company maturity, our aim is to give clients general benchmarks for providing the right amount of equity to executive and non-executive employees at the right time as they move toward an IPO event.

Assessing the Impact of Company Age

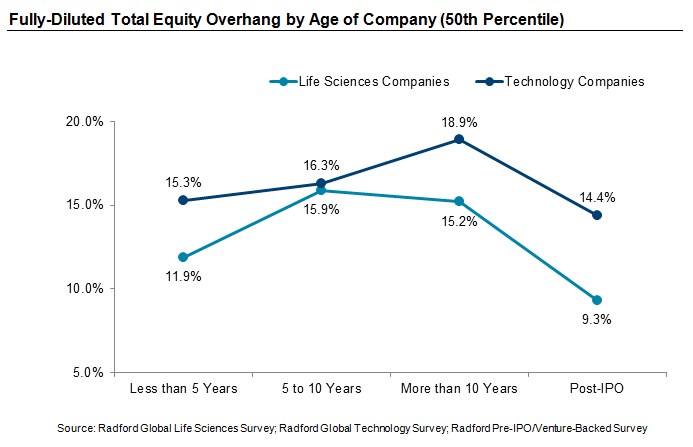

To analyze equity overhang and ownership levels based on a company's age, we divided companies into the following lifecycle segments: firms that are less than five years old, five to 10 years old, more than 10 years old, and immediately following an IPO (post-IPO).

At technology companies, the chart below indicates a steady increase in overhang levels the longer a private company operates. This makes plenty of sense — the longer a company is in existence, the more likely it is to grow its workforce and grant equity. In the run-up to a public offering, as many firms approach and surpass 10 years of age, overhang levels typically accelerate to support aggressive pre-IPO hiring.

A somewhat similar pattern is observed at life sciences companies, although increases in overhang levels are generally smaller and tend to occur earlier in the development of a company — between five to 10 years of age. Overhang levels also decrease dramatically at life sciences companies after they go public. From a research and development perspective, life sciences firms are typically at an optimal workforce level immediately following an IPO, and usually don't add significantly to headcount until they transition from pre-commercial to commercial.

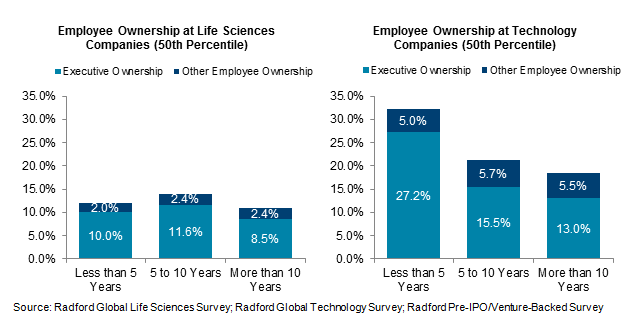

To further determine how equity grants change based on a company's age, we next turned to an analysis of equity ownership levels. Looking at the second set of charts provided below, which reflect equity ownership levels based on a company's years in operation, there are two interesting trends to point out: First, ownership levels increase slightly for non-executive employees in both sectors as companies grow older. And second, executive equity ownership levels tend to move in the opposite direction, dropping over time.

Let's discuss non-executive stock ownership first. The biggest jump in non-executive ownership occurs as companies move from less than five years old to between five and 10 years old. This suggests that more stock is being granted from the start-up phase to a more mature phase. The rise in broad-based equity ownership is reflective of the hiring trends we mentioned earlier, but there are also other likely factors at play. Companies may be granting more stock to existing employees as a retentive move to keep key talent engaged as a company moves into the sometimes murky, multi-year stage between launching as a fresh startup and getting serious about an imminent IPO. It also may reflect greater confidence in the ability to reward, motivate and retain high performers at truly competitive market rates.

When we turn to executive ownership levels, we need to focus on the technology and life sciences sectors more independently. At life sciences companies, executive ownership levels increase slightly before declining after 10 years of age. In this sector, the number of executives doesn't change significantly throughout a company's lifecycle, but neither does overall employee headcount. Unlike technology companies, there usually isn't the need to scale the business by adding multiple operations centers or hiring a large sales force —particularly when compared to pre-commercial biotechnology companies. Assuming research milestones continue to be achieved, life sciences companies are generally more stable when it comes to headcount.

The decline in executive ownership levels is far more pronounced at the technology companies we sampled. This could be a byproduct of more employees serving in senior leadership roles at technology companies as well as greater demand for private investment — both of which contribute to further dilution of executive equity stakes.

Invested Capital

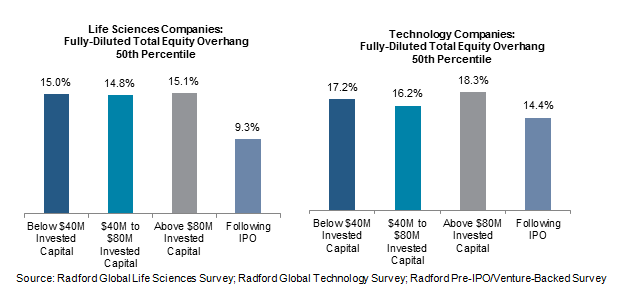

Next, we turn to how levels of invested capital influence the amount of equity issued to employees. Again, we look at overhang and equity ownership levels to see how equity grants fluctuate. When a company goes through a new round of financing, more stock is issued to the private investors; and in this regard, we would expect to see overhang rise. Indeed, that is the case, but only when outside investment levels reach above $80 million.

Immediately following the IPO, overhang falls as companies reign in the amount of equity they grant employees amid investor concern over dilution. Companies' equity grant behavior typically changes dramatically when they go public. Instead of granting stock options to all employees as a one-time event, equity is awarded in smaller amounts on an annual basis to a certain range of job levels. Post-IPO companies also find they can grant fewer shares since they have more tangible value to employees. The transformation shift in equity practices, combined with investor voting policies on equity ownership levels, push the level of overhang down as evidenced in the charts below.

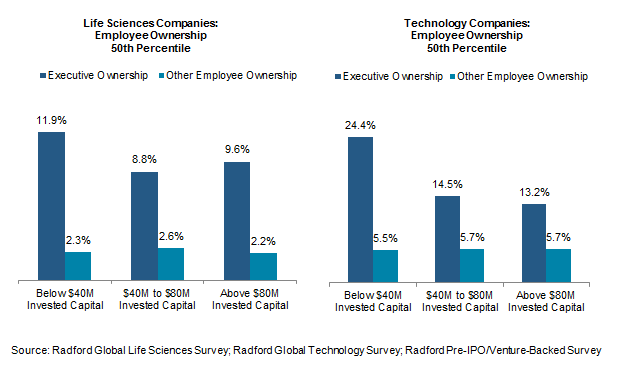

At the equity ownership level, we see the same trend for executives when we look at invested capital vs. company age. As the level of invested capital rises, executive ownership levels dip at both technology and life sciences companies. Again, the trend is more pronounced at technology companies because increased headcount at these firms has a larger impact on dilution levels.

Interestingly, investment levels do not significantly impact broad-based employees' equity ownership. Non-executive ownership levels dip only slightly at life sciences firms. At technology firms, ownership increases slightly before holding steady when investment levels peak. While more equity is being granted to venture capital firms and other private investors, employees' ownership levels remain relatively the same. This is attributed to a combination of two events: more employees are being hired as the company raises more money and builds its operations, and companies are offering employee make-up grants to counteract dilution following a round of financing. We suspect hiring activity accounts for a larger portion of the reason non-executives' equity ownership levels hold steady.

Conclusion

The important takeaway from our data analysis is not so much in the overall trend lines — for instance, we would expect overhang to rise as a company matures and then fall post IPO — it's in the details. When companies file a prospectus, nobody knows exactly how much outstanding equity the company has granted its employees. This figure typically ranges anywhere from 10% to 30%. Most prospective investors are satisfied with outstanding equity around 15%. We find overhang levels at the 388 pre-IPO technology and life sciences companies we studied fall within that range even as a company gets larger and closer to a public offering. The private firms we studied appeared to be effective at managing non-executive employee equity ownership so that it doesn't dramatically rise or fall based on a company's age or amount of investment. This will make changes to employee equity practices in a public setting an easier transition for both compensation professionals and employees.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.

Related Articles