Introduction

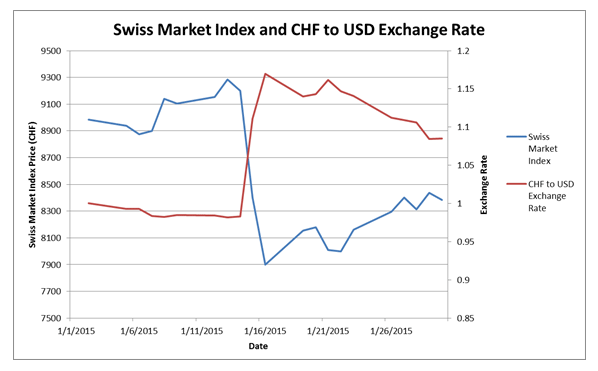

On January 15, 2015, the Swiss National Bank announced that the Swiss Franc (CHF) would no longer be connected to the Euro. In response to this announcement, the value of the Swiss Franc skyrocketed, as shown by the red line in the chart below:

In response to this spike in the value of the Swiss Franc, equities trading in Swiss Francs saw a sharp decline in their stock prices (as depicted by the blue line in the chart above). It's important to note that the underlying value of the companies listed on the Swiss Market Index did not change due to the currency announcement — all that changed was how their value was expressed.

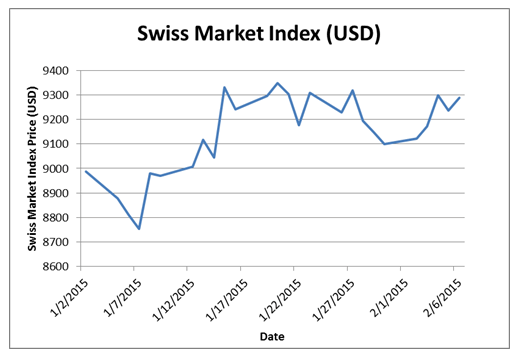

If we convert the Swiss Market Index from Francs to US dollars (USD), the large swing in the absolute price on January 15, 2015, is absent; see the chart below.

However, failing to account for the exchange rate fluctuation would put Swiss companies at a disadvantage, since only the drop in equity prices would be captured, while the surging strength of the Swiss Franc would be ignored. Conversely, companies trading in other currencies would gain an edge they do not deserve.

Currency Conversion Up-Close

The dramatic fluctuation the valuation of the Swiss Franc had on the Swiss Market Index illustrates an important point when designing relative TSR incentive plans that include foreign companies in peer groups. It is essential that companies convert foreign currencies into one common currency to remove outside influences that do not have any bearing on the underlying performance of peer companies.

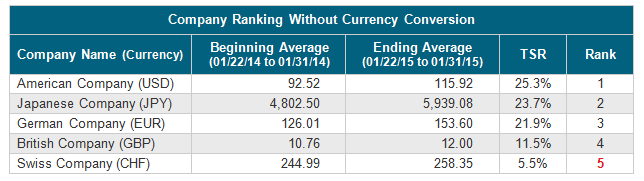

The recent situation with the Swiss Franc is not an isolated event. Albeit for different reasons, massive currency swings have also occurred in Argentina and Russia in the past few months. With that in mind, we decided to examine the potential impact of currency fluctuations using five large, global companies trading in US Dollars (USD), British Pounds (GBP), Euros (EUR), Japanese Yen (JPY), and Swiss Francs (CHF). The following table shows their one-year total shareholder return (TSR) ending on January 31, 2015, without conversion into a common currency.

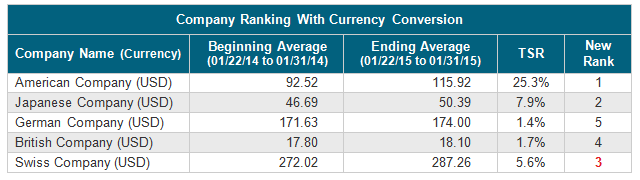

Now, the following table shows one-year performance for the same companies after converting all currencies to US Dollars:

After leveling the playing field, the Swiss Company moves from 5th to 3rd once it is no longer penalized for the increased value of the Swiss Franc, while the German Company slips from 3rd to 5th, reflecting the poor performance of the Euro over the measurement period.

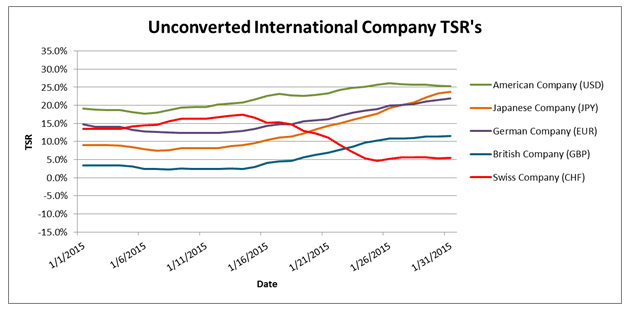

Putting the tables into a line graph, we can see just how dramatic the changes in stock price are between converting currencies and not. The following chart illustrates each company's TSR from January 31, 2014 through each day in January 2015, using 10-calendar day averages, without converting to a common currency:

Notice the general upward trend of the global economy and the contrasting nose-dive the Swiss Company's TSR takes following the January 15, 2015 announcement by the Swiss Bank. The next chart shows each company's TSR from January 31, 2014 through each day in January 2015, again using 10-calendar day averages, converting all companies to US Dollars:

After converting all currencies to the US Dollars, the Swiss Company is no longer penalized for the changing value of the Swiss Franc. Additionally, the US Company takes an even larger lead, due to the dollar's strong performance over the measurement period.

Conclusion

When dealing with relative TSR plans that contain international peers, it is important to consider the following points:

- The overarching goal of a relative TSR plan is to align the award holder's compensation with the value returned to shareholders

- Including international companies in a peer group implicitly states that the “value returned to shareholders” should be determined on a global scale

- Fluctuations in exchange rates are almost always out of a company's control, and often have little to no effect on the actual value of a company

In light of these points, we continue to believe it is essential to convert peer stock prices into a common currency before calculating TSR in order to neutralize the effect of variable exchange rates. In fact, the Association of British Insurers (ABI) supports this approach, stating in September 2011 that:

"Where TSR is used as a performance criterion and the chosen comparator group includes companies listed in overseas markets, it is essential that TSR be measured on a consistent basis. The standard approach should be for a common currency to be used. Where there are compelling grounds for the calculation to be based on local currency TSR of comparator group companies, then the reasons for choosing this approach should be fully explained."

Given the evidence provided by the latest situation with the Swiss Franc, it seems that the ABI's recommendation is validated once again. After all, the goal of relative TSR programs is to establish the fairest performance comparison possible — and now we see a real world example where the exclusion of exchange rates prevented that from happening. For more detail regarding the use of exchange rates in relative TSR plans, please see our whitepaper, Managing Relative TSR with Global Peers: The Impact of Currency Fluctuations.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.

Related Articles