One of the biggest challenges for compensation professionals in the run-up to going public is adapting your stock plan to meet public market expectations.

The window for going public opens and closes with regularity depending upon many factors, including the ease with which capital can be raised in either the public or private markets. There's no question that many private technology and life sciences companies are periodically evaluating whether they want to go public and when. One of the most important items on compensation professionals' checklist as part of that evaluation and preparation is making sure the veil is ready to be lifted on the employee equity plan. It's a process that can take several years of planning, and opportunities missed while private can be very costly once public.

Ensuring your stock plan is ready for its public debut can mean many things: measuring overhang and employee ownership, evaluating equity participation levels, and assessing your plan's compliance with regulatory requirements for public companies, to name just a few. While pre-IPO companies shouldn't expect their stock plan to align with public company equity award practices, measuring gaps in practices will help managers develop a roadmap as they approach the IPO and establish a new plan in conjunction with the offering. Our five-year study of companies in the Radford US Pre-IPO/Venture-Backed Survey found more than 90% of firms introduced at least one new equity compensation plan at, or very near the time of their IPO. This includes both equity incentive plans (EIPs) and employee stock purchase plans (ESPPs).

Differences in equity plans between private and public companies are driven by the tolerances and expectations among the different types of investors. Naturally, public company investors are more concerned about ongoing shareholder dilution. Pre-IPO companies tend to be more broad-based in their equity grants and utilize new-hire awards more often for all job levels.

To assist pre-IPO technology and life sciences companies on their journey to becoming public companies, we developed the following list of the top five areas of the employee equity plan that compensation professionals and managers should evaluate. Organizations benefit from analyzing the overall health of their equity plan and making necessary adjustments well before they have established an IPO date. Employees may be resistant to some of the necessary changes, but they become more palatable if they are phased in over time.

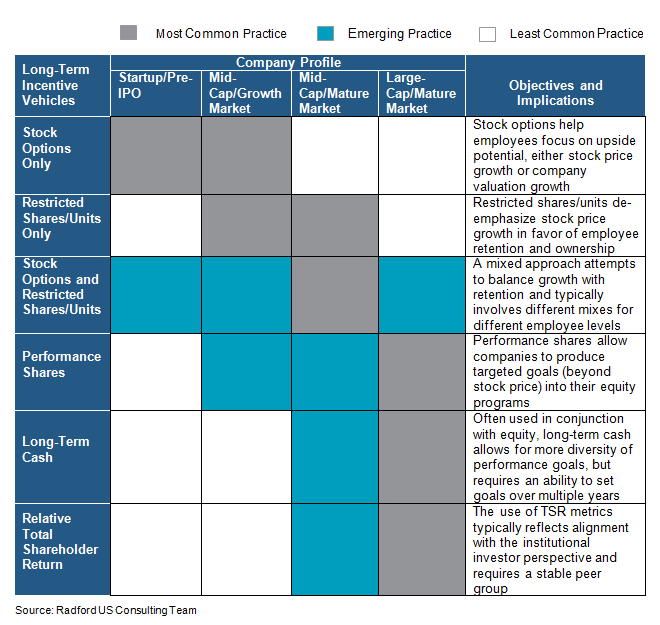

1. Different Types of Equity

One of the fundamental differences between long-term incentive (LTI) plans at private and public companies is the type of equity vehicles used. Pre-IPO companies need to assess the right mix of equity to use now and in the future. This mix will usually evolve— and, increasingly, this evolution is happening before the company even goes public. The chart below presents a comprehensive view of the different types of equity vehicles used by companies in all stages of development.

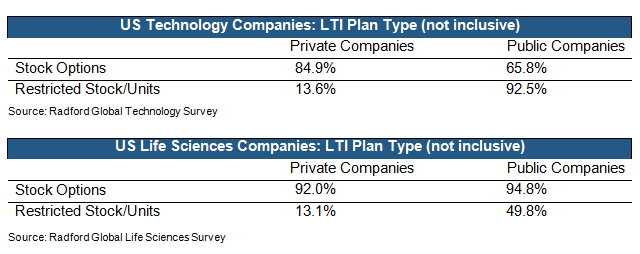

Private technology and life sciences companies tend to grant more options in their long-term incentive plans and far fewer restricted stock units (RSUs) or restricted stock. In a high-growth environment, stock options provide the greatest leverage to employees at the lowest cost to the company. As companies mature, and the growth in stock price moderates, the underlying value of the RSUs becomes more attractive. In addition, there is greater market pressure, especially in the technology sector, to migrate from options to RSUs (see our paper, RSUs Are Everywhere, But Are They Right For You?, for more details on this trend).

There are exceptions to this general guideline. RSUs are a great alternative for so-called unicorns — a nickname Silicon Valley has given to the growing number of private companies valued above $1 billion. When so much value has already been created, the worth of the underlying share becomes significantly more valuable to the employee. For these companies, RSUs do become an appealing alternative, but not without some challenges — primarily the tax consequences to an employee upon vest.

2. Total Equity Ownership

As we mentioned in the introduction, private companies should measure the amount of equity executive and non-executive employees hold against the total amount of outstanding shares. They must be prepared to explain and defend their employee ownership levels, particularly if they diverge from their peers' practices. While we typically think of employee ownership levels being higher at private companies, that's not always the case. If ownership levels are lower than the median point for the industry and size, companies may consider issuing "top-up grants" to certain employees and/or job levels before the IPO event.

To put ownership levels in perspective, we used the Radford Pre-IPO/Venture-Backed Survey and found total employee ownership at pre-IPO technology and life sciences companies is 20.9% and 15.5%, respectively, as of April 2015. Ownership levels will decline once public. In fact, as pre-IPO companies raise more capital, we already see employee ownership decline. Average employee ownership at technology companies that have raised under $40 million is 36.0%— falling to 22.7% once companies raise more than $80 million. For life sciences companies, ownership levels decline from 19.4% to 14.5%. These levels will continue to decline in the years following an IPO as incumbent employees exercise options at a faster rate than the company will be granting new shares.

3. Legal and Compliance Changes

Public companies navigate a myriad of tax rules and SEC requirements that private companies are exempt from. The Sarbanes-Oxley Act (SOX) followed by the Dodd–Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank) both contain provisions that address the treatment of stock plans. Dodd-Frank, for example, prohibits employees from hedging or pledging their company's stock. SOX restricts any employee, including officers of the company, from borrowing loans against their stock holdings.

Pre-IPO companies should assess how these types of requirements will impact their current stock plans and plan early for any changes that need to be made to bring plans in compliance. For example, private company plans generally include rights of first refusal, limitations on transfer, and different change-in-control and repricing provisions. On top of all that, the stock plan will need to be redrafted for exchange compliance and 162(m) compatibility.

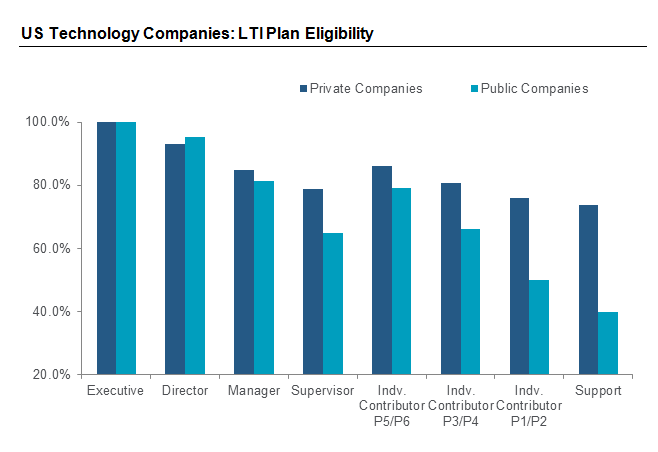

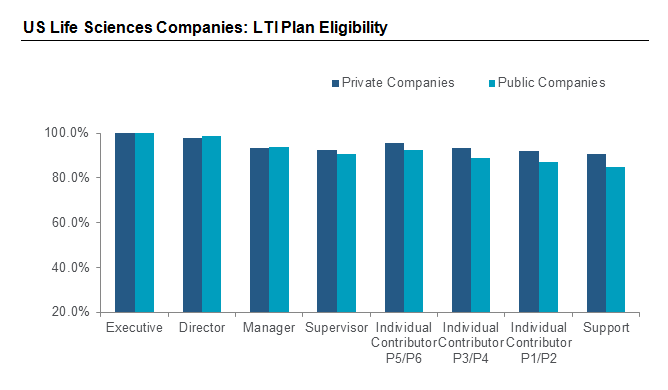

4. Employee Equity Participation

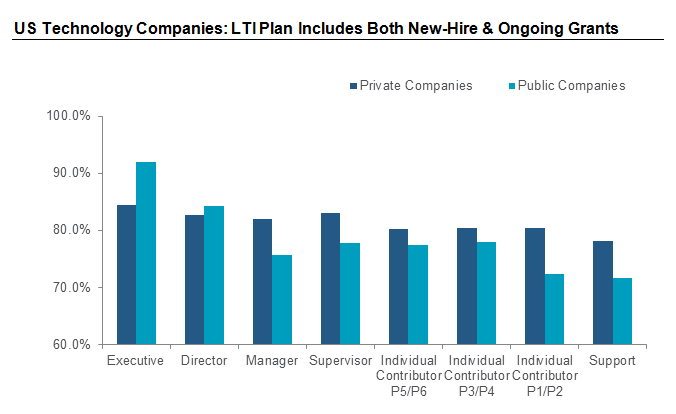

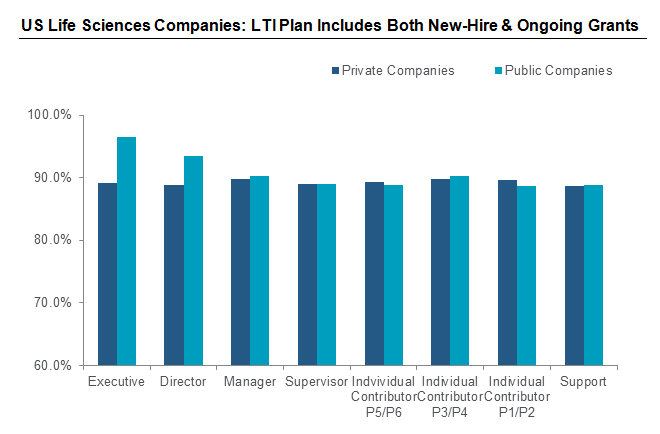

Private companies' approaches to LTI plan design are often different than public companies. As the charts below illustrate, private firms tend to offer new-hires a one-time stock award, while public companies will be more consistent with ongoing equity awards that are increasingly subject to certain performance conditions. This difference is most prominent at the executive and director levels, but the data becomes more mixed at lower job levels.

Private companies are more broad-based in their equity participation. Equity is a scarcer resource in the public setting because of shareholder dilution concerns; therefore, equity participation is more limited within the employee population to higher job levels.

Plan design is an area where there is potential for a phasing-in process combined with effective employee communication. HR managers should explain to employees how the company will transition to a continuous cycle of long-term equity awards either before or immediately following an IPO and what it means for each job level.

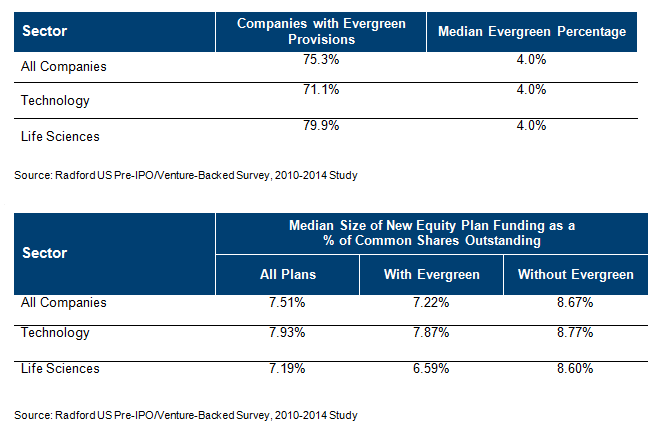

5. Equity Plan Funding and Evergreen Provisions

Lastly, it's important to determine the overall cost of the equity plan and how it will be funded. First, estimate how much of a hiring bump there's going to be post-IPO and how much equity is needed for new hires. This expense will usually spike in the first year of being public and slow down as your company matures and hiring activity returns to normal levels. Beyond new-hire grants, you'll need to evaluate the cost of ongoing grants. This relates back to our fourth point—ongoing grants are usually more consistent as a public company but smaller than the one-time awards needed to recruit employees to a startup company.

Once you have a good estimate of the cost to fund the equity plan, we encourage our clients to consider putting in place an evergreen provision since shareholders will rarely approve them after a company goes public. Plans without evergreen provisions typically need a larger initial pool of shares than those with built-in evergreen features. To highlight this point, the following table lists the initial size of equity plan funding (as a percentage of shares outstanding post-IPO) for plans with and without evergreen provisions.

For most companies, an evergreen plan will allow them to run their equity plans for up to five years without having to go back for shareholder approval. Equity pay plan proposals have come against greater scrutiny from Institutional Shareholder Services (ISS) and investors in recent years — causing the average percentage of shareholder support to decline.

Next Steps

There's lot of work to be done to prepare for an IPO. Evaluating your employee equity plan shouldn't be relegated to the last minute. Develop a roadmap and timeline for making changes to your employee equity plan, whether this includes shifting the equity mix and award cycles or prohibiting certain activities. Laying the groundwork early will ensure a smooth transition post IPO for employees— most of whom will be impacted in some way by necessary changes to long-term incentive plan design.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.

Related Articles