While companies face intense outside pressure to reduce the costs of administering broad-based equity plans, new research from Radford indicates that high-performing biopharmaceutical companies are actually aggressive users of equity

Introduction

Most companies believe certain types of compensation practices lead to better employee and corporate performance results. However, determining what kinds of practices are right for your industry and company can be difficult—particularly as your business evolves and stakeholders increasingly weigh in on the latest "best practices" in compensation. At the center of this discussion in the life sciences sector is equity compensation, and how to strike the right balance between underlying company culture, target pay philosophy, individual award competitiveness and aggregate levels of shareholder dilution.

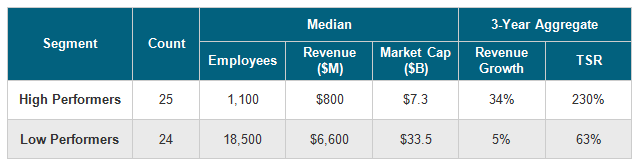

To address this topic, Radford set out to quantify the relationship between compensation practices and firm performance within the life sciences industry. We began with 49 biopharmaceutical companies in the United States (US) that have market capitalizations greater than $1 billion and revenues above $150 million. These companies were then separated into high performers ("Top Biopharma") and low performers based on three-year total shareholder return (TSR) and three-year revenue growth.

The differences are striking: Top Biopharma companies are vastly more productive and generate approximately $9.6 million in market value per person, compared to low performers who create around $2.2 million in market value per person. Per the chart below, Top Biopharma companies also had four times higher TSR and seven times greater revenue growth relative to the low-performing segment.

After researching pay practices at top and bottom performers, the results of our study yielded several insights that can be associated with better firm performance. One of our key findings is that companies with higher financial returns are more likely to grant employees larger amounts of equity and had higher participation in equity programs. Unfortunately, in an environment of increased pressure on dilution and more restrictive equity plan funding, this finding is directly at odds with current shareholder and proxy advisor thinking. This paper will examine the attributes surrounding equity programs among Top Biopharma companies in an effort to shed more light on potential factors that enable financial success.

The Current State of Play

Equity-based compensation is alive and well in the life sciences sector. With a significant number of recent IPOs, favorable market conditions and ongoing M&A activity, it's a good time to be an employee owner. However, the face of equity compensation has changed dramatically over the last few years, with evolving investor voting policies and more stringent limits used to evaluate dilution and equity plan cost.

One of the key themes emerging from our research is the disparate level of equity spend between high-performing and low-performing biopharmaceutical segments. Regardless of how equity is delivered, we see a consistent outcome: high-performing companies use more equity.

Before digging deeper, we would be remiss if we did not acknowledge the differences in size between our larger, low-performing companies and the relatively smaller, high-performing companies in our study. Just like the classic "chicken or the egg" dilemma, the question remains: Does size drive equity practice or does the choice of equity profile lend itself to a certain size of company? There are a number of interrelated issues that need to be addressed to fully flesh out this issue, which we won't tackle here.

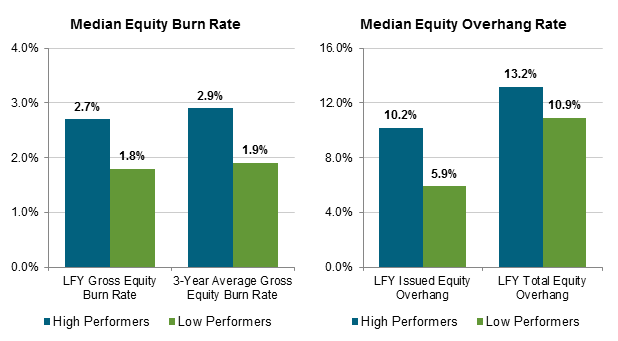

For now, our study simply takes performance levels and equity practices at face value, beginning with the burn rate and overhang charts below.

Based on our research, we find, in aggregate, that Top Biopharma companies grant equity at a rate of roughly 50% more than low-performing companies over both a one-year and a three-year average.

This finding is largely attributable to broader employee equity participation and the continued use of stock options at Top Biopharma companies, as well as more forgiving equity dilution norms among smaller companies. When looking over a multi-year period, we see high-performing companies actually increased their overall equity mix from around 55% stock options to 65% stock options in the most recent fiscal year. This suggests Top Biopharma companies are getting even more aggressive when it comes to dilution.

Digger Deeper: Equity Allocation, Participation and Mix

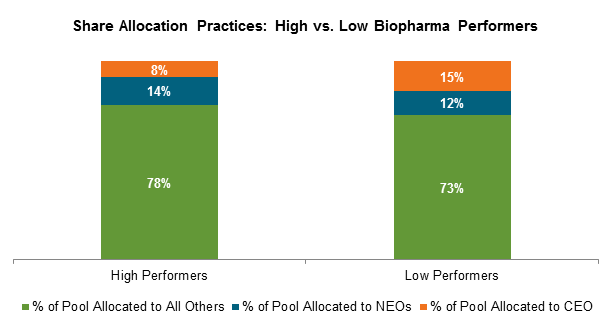

Once we began to explore equity practices in a more granular way across our high- and low-performing segments, several key themes emerged. First, when we look at the distribution (or allocation) of equity across the employee base, Top Biopharma companies deliver a higher concentration of equity to employees below the named executive officer ("NEO") level. Meanwhile, low-performing companies deliver a significantly higher concentration of equity to NEOs and chief executives.

This finding is explained, in part, by tighter constraints on equity plan costs at larger companies, including burn rate limits, shareholder value transfer guidelines and fewer shares available for grant per employee. Larger companies may also place a greater emphasis on cash compensation below the executive level. Still, the results are striking.

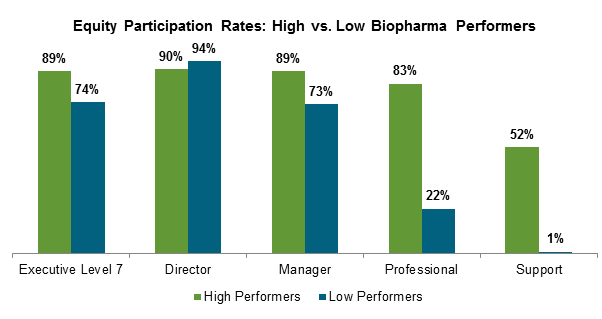

Moving along, when we examine equity participation rates, we again see fundamentally different patterns between high- and low-performing companies. Regardless of individual performance, equity is delivered broadly at Top Biopharma companies, with more than 80% of professional and 50% of support-level employees participating in annual equity programs. At low-performing companies, only 22% and 1% of employees in these respective levels receive annual equity grants.

There are several benefits to the approach observed at Top Biopharma companies. First, broader use of equity typically means that all employees have a common goal: to maximize their compensation opportunity by increasing shareholder value. This is a powerful tool that can shape culture and inspire all employees to "believe" in the organization's future success. Secondly, this approach requires less reliance on cash, providing companies more flexibility around investment choices, which is critical if they are not yet profitable. The chart below illustrates equity participation rates at high- and low-performing companies.

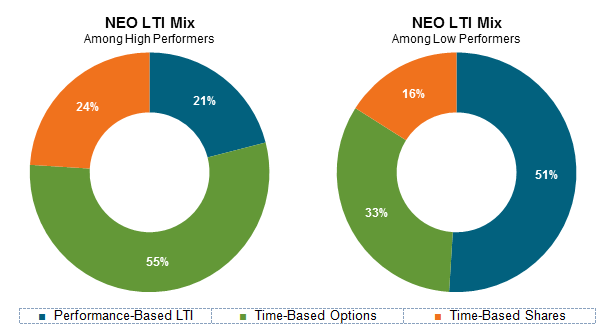

We've all heard the drum-beat of proxy advisors demanding more performance-based long-term incentives. And while many would agree with this approach in principle, an analysis of executive equity mix at high and low-performing companies reveals a counterintuitive result. NEO equity packages at Top Biopharma companies are weighted most heavily toward stock options (55% of the total value mix), followed in order by restricted stock (24%) and performance shares (21%). Meanwhile low-performers place the greatest emphasis on performance-based shares.

There are a number of ways to interpret this data, none which lead us to a conclusion that performance-based equity is misguided. Rather, low-performing companies could be embracing performance-based shares as a corrective measure to drive better performance in future years. Or, company size could again play a significant role. Smaller companies tend to favor plans with less administrative burden, which in this particular case translates into broad use of stock options at all levels, including executives.

Conclusion

Given the potential for extremely rapid growth trajectories and an increased focused on launching successful commercial products, life sciences companies thrive on flexibility and a reliance on equity over cash. As such, the industry shouldn't feel as pressured to conform to risk-averse, one-size-fits-all equity management trends. Namely, limiting equity vehicle choice and participation rates to reduce the costs of administering the plan. When it comes to life sciences companies, a more inclusive approach to equity compensation seems to make sense.

At the same time, we caution companies against taking the results of this study as a green light to implement a broad-based equity plan without first considering the stated goals of your equity program, your company constraints, and the impact of plan design on bottom-line and shareholders costs.

Increasingly, companies are looking to fit within the market norm, but also differentiate themselves from the pack with their pay programs. Consider making the case to your shareholders on why your company should grant additional equity to employees. With fact-based evidence on your side, shareholders may be persuaded that share dilution and higher burn rates (coupled with a smaller cash footprint) are a better alternative.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.

Related Articles