Introduction

Most life sciences companies face a shared compensation challenge: maintaining employee motivation during long, risky and uncertain product approval processes. These issues are particularly acute at early-stage pre-commercial companies, but they persist even as organizations grow. In both cases, drug development setbacks can have a major impact on employee morale and enterprise value.

To help meet this challenge, life sciences companies often rely heavily on equity compensation. Equity awards are inherently oriented toward long-term value creation, and provide employees with large upside potential when faced with uncertain product development outcomes. However, simply granting equity is not enough to attract and retain top employees in the midst of today's increasingly fierce competition for talent. Companies need to adopt the right equity programs at the right time to meet shareholder and employee expectations.

This task becomes increasingly complex as organizations globalise. Equity practices vary greatly by country, often out of legal necessity, and appropriate equity approaches can differ widely depending on employee level and function. Getting equity programs right – especially at scale – requires compensation professionals to understand a wide array of market inputs across multiple plan design issues. These issues include equity vehicle mix, equity value mix, receipt rates and performance metric selection. On top of these topics, public companies in nearly every mature economy face increasingly stringent corporate governance and regulatory requirements for share-based compensation and executive pay.

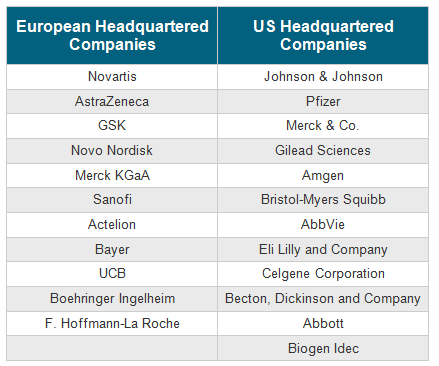

To begin unpacking all of these issues, Radford's team in Europe took a deep-dive into equity compensation practices at leading pharmaceutical companies in Europe and the United States (US). Comparing and contrasting equity practices at these companies is particularly powerful— they all have highly advanced and diverse equity programs, they invest heavily in understanding and assessing the latest market trends, and they compete globally for talent. Examining the choices these companies make on both sides of the Atlantic exposes critical equity strategy questions that life sciences firms at every stage of development should be asking.

Project Scope: Europe vs. the US

To initiate our analysis of pan-Atlantic equity compensation practices, we selected the following bellwether pharmaceutical firms headquartered in Europe and the US:

All of these companies share a few important characteristics. They have large operational and headcount scale, they have facilities in multiple countries, and they have the capacity to attract talent from Europe to the US and vice versa. Additionally, the fact that these companies are known to look at both European and US market data when designing global or localised equity plans is of special interest.

While some variations between our European and US groups will exist due to local regulatory and legal requirements, other contrasts across the Atlantic reflect meaningful differences between European and American compensation philosophies and approaches to pay-for-performance.

On this note, our analysis pays particular attention to performance-based equity and performance metrics. We offer fresh insights into how market-based and operational performance measures are used in both markets, and we also examine the tension between setting specific corporate performance goals and satisfying shareholder/governance concerns.

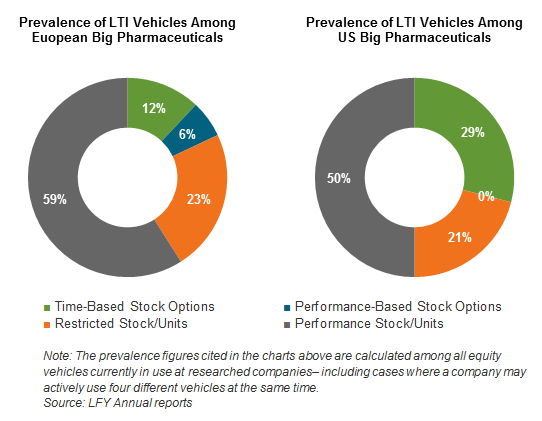

Equity Vehicle Mix

The equity vehicles currently in use in Europe and the US reveal several immediate differences in equity strategy across the Atlantic. First, time-based options account for nearly 30% of all equity vehicles in use in the US, more than double the prevalence observed in Europe. Second, European firms rely more heavily on performance-based equity.

The charts provided below illustrate the distribution of long-term incentive vehicles in use at our two groups of select pharmaceutical companies:

The reduced use of stock options in Europe is primarily related to various corporate governance initiatives in individual countries and broader European Union directives. As a result of regulatory actions, most of European pharmaceutical companies have abandoned options entirely. Companies that continue to resist this trend in Europe face ongoing shareholder criticism. As Radford's recent article on long-term restricted stock unit (RSU) adoption trends in the technology and life sciences sectors points out, US companies are following suit for many of the same reasons, but at a slower pace, especially in the life sciences sector.

The choice of when and where to grant specific equity vehicles should not be governed solely by market norms or shareholder desires. Companies should consider their specific growth goals and other important pros and cons associated with any equity vehicle choice. For stock options, this means weighing the pros of simple plan design against the cons of potentially volatile incentive outcomes and higher shareholder dilution rates. For performance shares, this means weighing the positives of broader shareholder acceptance against the negatives of greater plan design and communication complexity.

Equity Value Mix

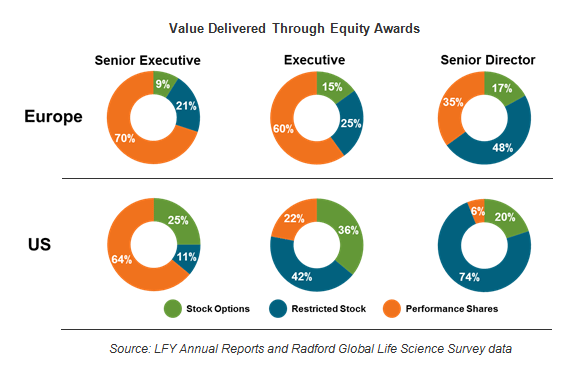

Prevalence data only tells us if certain equity vehicles exist within a market— it's a simple yes or no proposition. However, equity value mix data hints more directly at the relative importance of equity vehicles within a company's compensation strategy. Looking at equity value mix across the Atlantic, Radford data reveals both surprising and expected trends among leading pharmaceutical companies.

In both Europe and the US, equity value mix for senior executives (i.e., C-suite leaders and executive directiors) is quite similar; roughly 65% to 70% of equity value is delivered via performance shares (see the following charts). This data points to the strong influence of regulators and shareholders in both markets, who continue to demand tighter links between pay and performance. We also believe another force may be at play. When it comes to senior executive talent, mobility and competition rates are high. The market for talent is truly pan-Atlantic, and so too are compensation practices.

Looking lower into organisations (at the Vice President and Senior Director levels), many of the differences one might expect to see between Europe and the US begin to emerge. Leading pharmaceutical companies in Europe continue to rely heavily on performance shares, while US firms rapidly deemphasize performance shares in favour of stock options and restricted shares/units. Several factors may contribute to the data we observe in the US, including:

- US companies continue to believe strongly that stock options are an important and effective pay-for-performance vehicle, and face less investor pressure than their European counterparts to push performance shares deeper into their organizations;

- US companies are more likely to believe lower-level executives and employees have less influence (i.e. "line of sight") over the metrics and goals tied to performance shares; and

- Given that the adoption of broad-based restricted stock unit programs in the US is accelerating, companies feel competitive pressure to emphasize RSUs as high up into their organizations as possible.

Depending on the specific situation at your company, including its stage of development and micro-region (e.g., the San Francisco Bay Area vs. Boston vs. London vs. Medicon Valley), all or some of these drivers may be true.

Finally, our data on equity value mix at the executive and senior director levels points to an interesting challenge companies may face when recruiting talent across the Atlantic. Not only do companies need to create competitive offers in terms of value, they may also need to translate that value into new or different equity incentive vehicles. This change may not always be a welcome one, especially if the change is from RSUs in the US to performance shares in Europe.

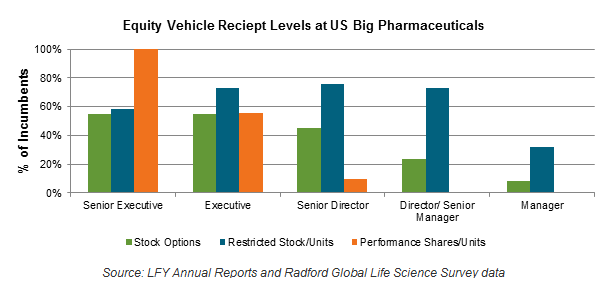

Equity Program Participation

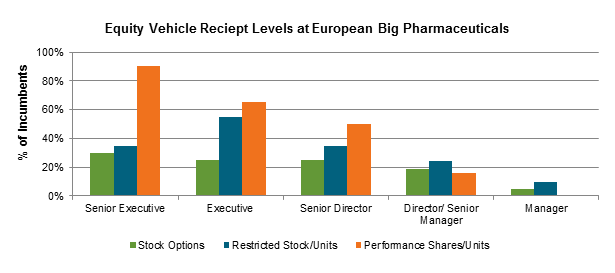

The next layer of our analysis examines equity program participation rates: who gets equity and who doesn't. In broad strokes, the Radford data presented in the charts below points to two significant differences between big pharmaceutical companies in Europe and the US. First, equity participation rates among European employees at nearly all levels are lower. And second, aligning with the data we just shared on equity value mix, European firms push performance shares much more deeply into their organisations.

These findings point to a number of fundamental strategic questions, including:

- What equity strategy will most effectively drive long-term performance: granting equity to a broad set of employees as is the case in the US, or granting equity to targeted employees as is the case in Europe?

- Where in an organisation does it make sense to shift the emphasis of equity incentives from driving specific performance results to overall employee retention? In Europe, that line appears to be managers. However, in the US, the line is currently drawn fairly sharply at the executive level.

The differences in European and US equity compensation philosophies illustrated in the charts above force us to return to the issue of line-of-sight in performance equity plans and performance metrics, which we examine in the section below.

Performance Measures

Determining the "right" or "best" performance measure for your company is always a hotly debated topic. Even when extensive market data is consulted, companies are often prone to second-guessing, either internally by employees, or externally by shareholders. It's a complex matter, especially when comparing and contrasting practices in Europe and the US.

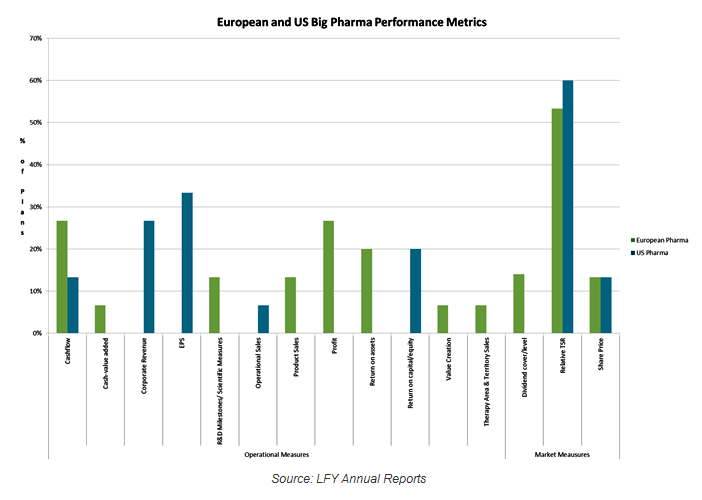

In terms of similarities between major pharmaceuticals on either side of the Atlantic, one point of performance metric consistency stick outs— relative TSR is by far the most common metric in both markets. This trend is a reflection of increased pan-Atlantic focus on pay-for-performance issues and the advent of regular Say-on-Pay voting. However, as the chart below demonstrates, this is where the metric selection similarities end.

In Europe, outside of relative TSR measures, big pharmaceutical companies tend to place a heavy emphasis on operational metrics such as profit, return on assets, and value creation. In the US, relative TSR is dominant, followed by earnings per sharing (EPS) and overall corporate revenues.

Interestingly, big pharmaceutical companies in both markets behave in roughly the same manner when it comes to combining operational and market-based metrics— 40% of firms in both markets use a combination of measures.

Using a combination of market-based and operational performance measures has advantages. First, companies can balance their specific performance goals with broader shareholder interests, and second, operational measures serve as excellent payout "modifiers" in the event that market-based measures produce results that might be viewed as disconnected from core business results.

Balancing issues of performance metric selection, deployment and weighting is critical. For public pre-commercial biopharma companies, relative TSR is less relevant; these companies are usually better off focusing on operational metrics tied to the product milestones that will drive value creation. Conversely, a market-based metric, or a combination of market-based and operational measures, makes more sense for big pharmaceuticals.

Conclusion

Our exploration of equity incentive practices across the Atlantic raises important strategic questions about the intent, value and efficacy of equity compensation. By comparing and contrasting Europe and the US, some of these issues come to light in new ways. Our data also points to the many potential challenges inherent in attracting and retaining talent from global competitors, especially where practices vary significantly between Europe and the US.

Beneath a surface layer of similarities, significant differences between Europe and the US begin to emerge. European companies tend to favor the use of performance-based equity deeply within their organizations, and use equity more sparingly at all employee levels. Meanwhile, US companies tend to limit performance shares to vice presidents and higher, focusing on retention issues with broad-based RSU grants. And in terms of the performance metrics tied to equity grants, while both markets have bowed deeply to investor sentiment by using relative TSR; in Europe, a wider diversity of operational metrics are also in play. These differences sit on top of other variations in practice between Europe and the US, such as phased vs. cliff vesting, and post-vesting holding periods, which are more prevalent in Europe relative to the US.

In today's current governance environment, it is easy to follow market practice and take controversial practices off the table. This happened long ago to share option plans in Europe. However, conformity to a one-size-fits-all model, where for example, relative TSR is adopted by a company simply because it is the most prevalent metric in the market, may not actually reflect what is needed to drive top notch performance at that specific company. There is no silver bullet when it comes to metric selection; however, specific industry and company drivers should probably receive greater attention than they do today. On this basis, it may be worth considering performance equity plans with a higher weighting tied to criteria such as scientific measures, including the development of new molecular entities, the volume of entities brought to phase II or III trials, R&D development, or key approval milestones.

There is a prevailing attitude in both Europe and the US that shareholders will vote down proposals that are not entirely "compliant." It is important to remember that incentive plans are designed to achieve the objectives we outlined earlier – that is, to drive performance in the context of uncertain product development and approval timelines. Investors remain aware of this. A well thought out and well documented equity plan proposal, combined with effective consultation will strongly influence the debate and go a long way toward securing equity incentive plans that are fit for purpose for the sector generally and the company specifically.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.

Related Articles